SFDR translation errors that increase ESMA greenwashing risk

- Apr 7

- 9 min read

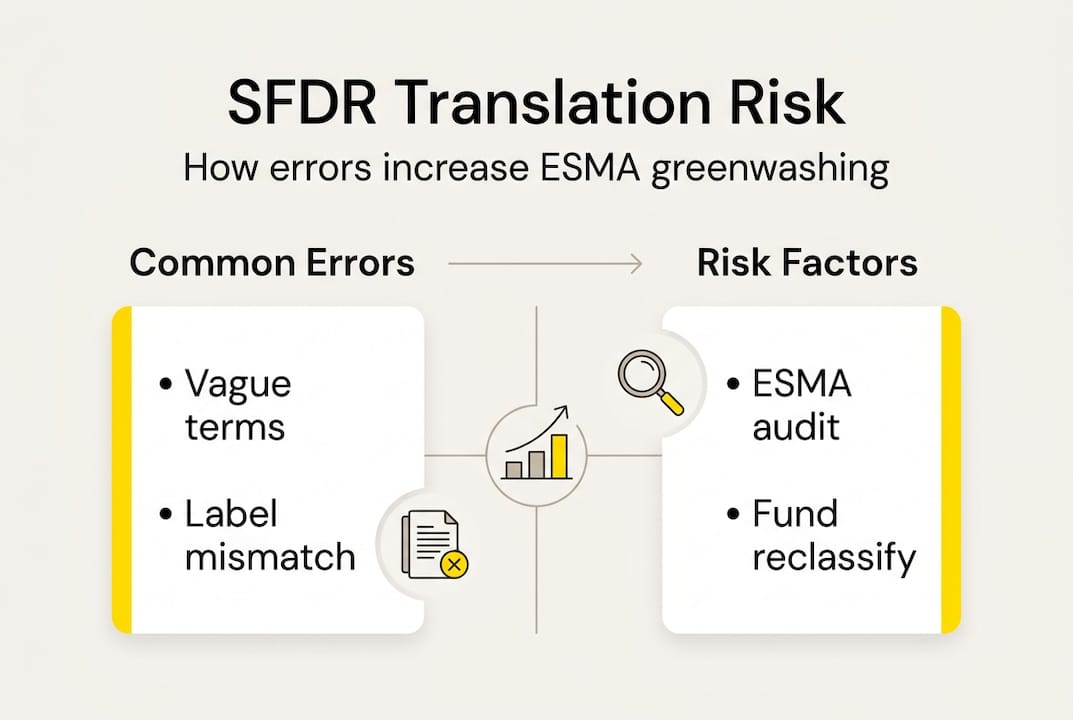

Translation inconsistencies of key SFDR terms pose significant compliance and greenwashing risks.

ESMA proactively enforces language quality, flagging vague or mismatched disclosures across documents and languages.

Preparing for SFDR 2.0 requires robust translation governance to maintain regulatory clarity and avoid reclassification.

When over €175B in funds were reclassified from Article 9 to Article 8 between 2022 and 2023, the industry treated it as a data governance story. It was also a translation story. Vague, inconsistent, or poorly localized disclosures created the ambiguity that regulators then acted on. ESMA’s 2025 Common Supervisory Action (CSA) found widespread deficiencies in how sustainability claims were worded across markets. This article explains where translation errors enter the SFDR disclosure chain, why specific terminology traps like “sustainable investment,” “do no significant harm,” and “principal adverse impacts” are particularly dangerous, and what compliance-focused asset managers need to do before the next regulatory review cycle.

Table of Contents

Key Takeaways

Point | Details |

Translation errors are material | Improperly translated SFDR disclosures directly increase ESMA enforcement and greenwashing risk. |

ESMA targets language | ESMA and NCAs scrutinize not just content but precision across all language versions of disclosures. |

Mitigation is achievable | Cross-jurisdictional template alignment and expert localization can drastically reduce compliance exposure. |

SFDR 2.0 changes the bar | Upcoming regulations will require even stricter translation governance—acting early avoids forced fund reclassification. |

Why translation errors matter under SFDR Article 8 and 9

SFDR Article 8 covers funds that promote “environmental or social characteristics.” Article 9 applies to funds with a “sustainable investment objective.” Both definitions are precise in the original regulatory text. But when those definitions travel across 24 EU official languages, through prospectuses, KIIDs, annual reports, and marketing materials, precision erodes fast.

The core problem is that SFDR was never designed with translation governance in mind. The regulation assumes that the meaning of terms like “sustainable investment,” “do no significant harm” (DNSH), and “principal adverse impacts” (PAI) will remain stable across jurisdictions. In practice, they do not. A linguist without financial regulatory training may render “promotes” in Article 8 as a weaker or stronger term than intended, shifting the implied commitment of the fund. That single word can determine whether a disclosure reads as Article 8 or Article 9 territory.

SFDR disclosures expose managers to greenwashing risk precisely because of label misuse, vague language, and poor quality disclosures. These are not abstract risks. They are enforcement triggers. ESMA and national competent authorities (NCAs) now treat disclosure language as evidence, and inconsistency between language versions of the same document is read as a red flag.

For managers operating across multiple EU markets, MiFID II disclosure translation compliance adds another layer of terminology that must align with SFDR language. A mismatch between how “ESG objective” is described in your MiFID II suitability documentation versus your SFDR pre-contractual disclosure can itself become a compliance issue.

Translation error type | Compliance risk | Regulatory consequence |

Ambiguous rendering of “promotes” | Article 8/9 boundary blur | Reclassification, investigation |

Generic DNSH language | Fails RTS specificity test | Disclosure rejection, scrutiny |

Inconsistent PAI terminology | Cross-document mismatch | Greenwashing flag by NCA |

Boilerplate ESG claims | No binding criteria evident | Enforcement action, fine |

Marketing vs. disclosure misalignment | Misleading investor communication | Regulatory sanction |

Common error patterns include:

Using generic sustainability vocabulary instead of the exact SFDR-defined terms

Translating “binding criteria” loosely, removing the obligatory character of the commitment

Rendering “principal adverse impacts” as a general concept rather than the specific PAI framework under the RTS

Inconsistent treatment of the same term across the prospectus, KIID, and website versions

Managers who underestimate localization risk in EU fund documentation are the ones most likely to face reclassification pressure. The €175B reclassification wave was not caused by bad investment strategies. Much of it was caused by disclosures that could not withstand regulatory scrutiny.

Regulatory focus: How ESMA detects and enforces against greenwashing

ESMA does not wait for investor complaints. Its enforcement model is proactive, coordinated, and increasingly focused on disclosure language quality. The 2023 and 2024 CSA exercises made that clear: vague disclosures, portfolio mismatches, and poor data governance were the primary findings across participating NCAs.

“ESMA enforcement focuses on disclosure quality: inconsistencies, inadequate DNSH and PAI coverage, generic language, and misalignment between marketing materials and regulatory filings.” This is not a future risk. It is the current enforcement standard.

Here is how the enforcement sequence typically unfolds:

Disclosure review. NCAs compare filed pre-contractual templates (Annex II or III under the RTS) against marketing materials and website content in each local language.

Inconsistency flagging. Any divergence between language versions, or between disclosure and marketing text, is logged as a potential greenwashing indicator.

Data and methodology check. Regulators verify whether PAI statements and DNSH assessments are substantiated by actual portfolio data, not just translated boilerplate.

Escalation. Where inconsistencies are material, the NCA escalates to a formal investigation. ESMA coordinates findings across jurisdictions.

Enforcement action. Outcomes range from mandatory reclassification to public censure and financial penalties, depending on the severity and jurisdiction.

Poor translation and generic text are now treated by ESMA as immediate greenwashing risk factors. A fund that files an Article 9 disclosure in English but whose German or Polish version softens the sustainability objective language is exposed, even if the English original is technically compliant.

For managers also navigating Basel III/IV translation requirements, the lesson is the same: regulatory terminology is not interchangeable, and cross-language consistency is a compliance obligation, not a stylistic preference.

Pro Tip: Before any regulatory submission, run a parallel review of all language versions against the approved ESMA disclosure templates. Flag any term that deviates from the official regulatory glossary, even if the deviation seems minor. Regulators notice.

Where translation errors happen: Real-world fund disclosure pitfalls

SFDR compliance touches multiple document types simultaneously. Each one is a potential failure point.

The pre-contractual disclosure (Annex II or III of the RTS) is the most scrutinized. Generic or boilerplate language in these templates is an immediate trigger for regulatory review. When a fund’s French Annex II uses “favorise” (favors) where the English version uses “promotes,” the implied strength of the ESG commitment shifts. That shift matters to ESMA.

Annual and periodic reports carry PAI statements that must be quantified and consistent across all language versions. Translating “principal adverse impacts” as a generic phrase about negative effects strips the term of its regulatory meaning and its link to the mandatory PAI indicators under the RTS.

Document type | Well-localized example | Poorly translated example | ESMA risk level |

Pre-contractual disclosure | Exact RTS terminology, binding criteria explicit | Vague “ESG-friendly” language | High |

PAI statement | Specific indicators named, quantified | Generic “we consider impacts” | High |

KIID/KID | Consistent with prospectus terminology | Different ESG vocabulary used | Medium |

Website/marketing | Mirrors disclosure language precisely | Broader sustainability claims | High |

Breakdowns cluster around three specific terms. “Promotion” under Article 8 must read as an active, binding commitment, not passive aspiration. DNSH must be translated with its full conditional logic intact: the fund does not significantly harm any other environmental or social objective. PAI must retain its technical character as a defined set of indicators, not a general concept.

To reduce exposure, compliance teams should follow these remediation steps:

Build a fund-specific term base covering all SFDR-defined terms in every target language before any document goes to translation.

Require translators to work against approved ESMA templates and flag any deviation for legal review.

Run a cross-document consistency check after translation, comparing terminology across the prospectus, KIID, PAI statement, and website.

Document the translation review process for audit purposes. ESMA expects evidence of governance, not just compliant output.

Treat terminology errors in contracts and disclosures as equivalent risks, because regulators do.

Managers who have experienced translation errors in compliance documents in other regulatory contexts will recognize the pattern. The fix is always the same: governance before translation, not correction after filing.

Future proofing: SFDR 2.0, evolving standards, and practical compliance strategies

The European Commission’s SFDR 2.0 proposal, published in November 2025, replaces the Article 8 and 9 framework with three new categories: Sustainable, Transition, and ESG Basics. The explicit goal is to fix the labeling misuse that the current framework enabled, shorten disclosure documents, and reduce the ambiguity that translation inconsistencies exploited.

For translation and compliance teams, this is both an opportunity and a deadline. The new categories carry their own defined terminology, and that terminology will need to be governed just as carefully as the current Article 8/9 language. Research on Article 9 greenwashing reduction confirms that clearer categorization reduces but does not eliminate the risk of misrepresentation. Translation governance remains the critical control.

The practical implication is that managers who have not yet built robust translation workflows for SFDR will face a double transition: updating their disclosures for the new categories while also trying to fix the terminology inconsistencies that already exist across their current filings.

Immediate action steps for compliance teams:

Audit existing translated disclosures now, before SFDR 2.0 implementation timelines are confirmed, to identify terminology gaps.

Map current Article 8/9 language to the proposed Sustainable, Transition, and ESG Basics definitions to understand where reclassification may be required.

Establish a translation governance policy that assigns accountability for terminology decisions at the compliance officer level, not just the translation vendor level.

Align your term base updates with the final SFDR 2.0 regulatory text as it progresses through the legislative process.

Review how translation under EU MDR and other regulated frameworks handle terminology governance, since the structural approach transfers directly to SFDR.

Pro Tip: Do not wait for SFDR 2.0 to be finalized before updating your translation governance. The managers who start harmonizing disclosure wording now will avoid the scramble that follows every major regulatory transition.

Why translation is the real ESG test ESMA cares about

Most compliance discussions about SFDR focus on data: PAI indicators, taxonomy alignment percentages, DNSH methodologies. That focus is understandable. But it misses where enforcement actually lands.

ESMA does not fine funds for having imperfect ESG data. It flags funds for saying one thing and meaning another, across languages, across documents, across markets. The cross-border prospectus risk is not theoretical. It is the mechanism by which good-faith ESG strategies become greenwashing allegations.

Organizations that invest heavily in ESG research and portfolio construction but treat translation as a vendor cost to minimize are the most exposed. They have the substance but lose it in the language. That is a board-level compliance failure, not a back-office mistake.

Translation governance should sit alongside data governance in your SFDR compliance framework. The same rigor you apply to PAI data sourcing should apply to how “principal adverse impacts” is rendered in every language version of every disclosure. ESMA has made clear that it reads both.

How expert localization partners help safeguard your SFDR compliance

For asset managers operating across EU markets, the gap between compliant intent and compliant output often comes down to the quality of the translation process itself.

AD VERBUM’s AI+HUMAN hybrid workflow integrates your existing term bases and translation memories before any document is processed, ensuring SFDR-specific terminology is enforced from the first output. Finance-specialist SME linguists then review every translation for regulatory accuracy, not just linguistic fluency. The process is QA-aligned to ISO 17100 and ISO 18587, and all processing runs on EU-hosted infrastructure under ISO 27001 certification, supporting your data sovereignty requirements. If you are preparing for SFDR 2.0 or addressing gaps flagged in a CSA review, explore AD VERBUM’s specialist localization services or contact the regulatory language team directly for a tailored consultation.

Frequently asked questions

What are the main translation errors in SFDR Article 8 and 9 disclosures?

Ambiguous terminology, inconsistent application across documents, and direct mistranslation of regulatory concepts like “sustainable investment” and “do no significant harm” are the most common and highest-risk errors. These errors are treated as greenwashing indicators by ESMA and NCAs.

How can translation errors actually expose asset managers to ESMA greenwashing enforcement?

Inconsistent or vague translated disclosures are flagged during CSA reviews as greenwashing risks, which can trigger formal investigation and forced fund reclassification. The enforcement mechanism is direct: language quality is treated as evidence of intent.

What is SFDR 2.0 and how does it impact translation requirements?

SFDR 2.0, proposed in November 2025, replaces Article 8 and 9 with three new fund categories and will require precise, consistent translations of the new category definitions across all disclosure documents and markets.

What practical steps should asset managers take right now to reduce SFDR greenwashing risks from translation errors?

Build a fund-specific regulatory term base, align all language versions against approved ESMA templates, require SME review of every translated disclosure, and document the entire translation governance process to demonstrate compliance during regulatory review.

Recommended